Trade, Tariffs, and the USD Convenience Yield

Tariffs will likely keep interest rates high, increase the risk of the US Dollar, and potentially sponsor a global re-positioning away from US equity markets

The last 10 years of market history have been marked both by the dominant outperformance of American large-cap stocks and by contrarian investors highlighting the statistical irregularity of the ongoing regime. Without a countervailing force, this type of irregularity can persist for a very long time. Today, I believe that force has emerged: the USD convenience yield, which typically benefits unhedged foreign investors in a risk-off environment, appears to be disappearing. Empirical evidence shows that differences in country-level interest rates and currency risk premia are linked to trade flows. Countries heavily involved in global trade tend to have lower average interest rates and safer currencies. Interest rates and U.S. Dollar risk are likely to increase with the severity of tariffs and could potentially drive a global repositioning away from U.S. equity markets.

Figure 1 shows the average relative max drawdown of the S&P 500 in USD against the max drawdown of the S&P 500 denominated in an equal weighted average of GBP, EUR, and CAD. During both COVID and the recent 2022 bear market, unhedged foreign investors enjoyed +2% and +11% less severe drawdowns relative to their hedged counterparts. As the VIX rises modestly today, the crisis benefit of USD convenience yield appears to have vanished.

Figure 1: Average Relative Max Drawdown SPY USD vs. Unhedged Foreign Base FX

Source: S&P Capital IQ, Countervail Analysis

Historically, the US stock market has offered international investors a positive-carry hedge on consumption risk priced in their local FX. In other words, when global markets decline, the dollar appreciates relative to other currencies, protecting foreign investors’ local purchasing power during bad times. This has made the US equity market a very attractive place to park foreign money.

There are early indications that this benefit has now weakened, and empirical data support the idea that a restrictive tariff regime would place it under further jeopardy. Research by Richmond (2016) pinpoints trade centrality as a key driver of country-level differences in interest rates and currency risk premia. The countries that are most densely connected to global trade tend to be more exposed to global consumption growth shocks, which causes the currencies of these countries to appreciate in bad times. This results in lower interest rates and lower currency risk. Figure 2 shows a stylized depiction of our global trade network, where links are measured by bilateral trade intensity and circle position corresponds to trade network centrality. Central countries like Singapore have lower average interest rates and safer currencies while peripheral countries like Mexico and New Zealand tend to have higher average interest rates and riskier currencies.

Figure 2: World Trade Network, 2013

Source: Trade Network Centrality and Currency Risk Premia (Richmond, 2016)

To the extent that tariffs reduce the centrality of the US position in global trade, Richmond’s research suggests we should expect both higher interest rates and an increase in the riskiness of the US dollar. The potential for US Dollar devaluation arrives at a time when aggregate valuations remain stubbornly high, the Fed’s ability to defend the dollar with higher short rates is limited, and the US weight in global equity indices is stretched to the extreme. In fact, I struggle to think of a more consensus view than an out-sized allocation to US equity markets.

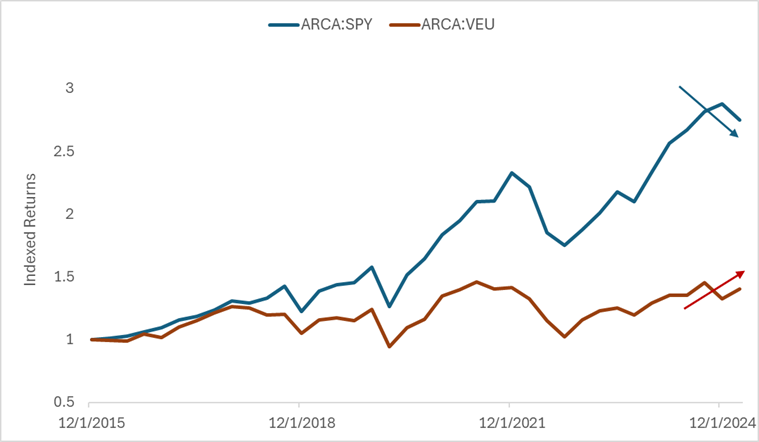

Gabaix and Koijen (2021) document that markets are surprisingly inelastic: a $1 investment in the stock market increases the market’s aggregate value by about $5. As international portfolios increasingly tilted toward American-listed assets, prices for those assets would have increased even more. Figure 3 shows the index performance of the S&P 500 relative to the all-world ex-US index since 2015.

Figure 3: S&P 500 vs. Rest of World (ARCA:VEU), December 2015 – Present

Source: S&P Capital IQ

With the AI bubble deflating, I’m now most concerned about the potential for contemporaneous declines in U.S. equity markets and the dollar, which could drive a feedback loop where international investors increasingly reposition away from the U.S. To be clear, I’m neither calling for the end of the USD as the world reserve currency nor the ‘end of U.S. exceptionalism’. Rather, I see considerable cyclical pressure on the mechanism that has driven relative U.S. benchmark outperformance over the past ten years. The inelastic nature of markets would only amplify this course correction. Of course, this is far from guaranteed, and in practice, it’s possible that the current tariff policies won’t meaningfully disrupt U.S. trade centrality. But as most strategists seem to monitor economic and policy news, I’m paying very close attention to the DXY-SPY correlation. The forces that conspired to drive relative U.S. equity market dominance for the past decade are likely best measured with this relationship, which may be at the early stages of unwinding.