Lobbying, Regulation, and Equity Returns

Theory, empirics, and anecdotal data show that lobbying dollars can create alpha opportunities

Since 2000 there have been four ‘Farm Bills’ that authorized a cumulative $750 billion in agriculture related subsidies. A broad consortium of grain traders, commodity associations, crop insurance companies, equipment manufacturers, and food processors collectively spent an estimated $173 million lobbying the 2008 Farm Bill, which alone generated $88 billion in subsidy outlays across commodity, insurance, and conservation programs. Empirical studies show a positive relationship between lobbying efforts and the stock returns of businesses driving them – evidence in favor of the idea that regulatory outcomes are products for firms as opposed to safeguards for the public. I highlight a recent inflection in lobbying spending among broadcasters, where valuations are near historical lows, but favorable regulatory changes have begun to materialize.

While most would likely believe that regulations are designed to benefit and protect the public, Stigler (1971) developed an alternative view: firms and industries acquire regulatory outcomes from politicians. Firms compete in the political arena – typically by hiring lobbyists – to promote their own interests, create entry barriers, and thwart competitors. In other words, regulation is just another product to be bought and sold. While the 2008 Farm Bill cost $173 million to lobby in congress, it generated an $88 billion subsidy program – an ROI that should be eye-watering enough for corporate managers to abandon their competitive strategy textbooks and head straight to the capitol with a fistful of dollars. The Farm Bill is just one instance of a large bi-partisan industry where dollars are exchanged for regulatory outcomes. Figure 1 shows the largest spenders on lobbying from 1998 - 2024. Firms in pharma, aerospace and defense, insurance, communications, and broadcasting have spent hundreds of millions of dollars over the past two decades to negotiate favorable policy outcomes.

Figure 1: Top Spenders on Lobbying, 1998 - 2024

Source: Opensecrets.org

One basic public-interest argument for regulation is to prevent monopolies, which form naturally when a single firm minimizes the cost of a product, eventually allowing it to charge higher prices and earn excess profits. Broadcasting, while not a true natural monopoly, does have some monopoly-like characteristics: building and operating a TV station has high fixed costs and serving the incremental viewer costs very little. Today’s media industry is generally competitive, but monopoly characteristics become more pronounced in smaller markets where a single broadcaster may operate the only local newsroom. For this reason, the FCC has rules in place to prevent single broadcasters from gaining too much market power at either the national or local level. Nationally, the FCC limits broadcaster ownership to 39% of US households. Locally, the FCC restricts the number of stations a single broadcaster can own in a single market, typically limiting a broadcaster to one of ABC, CBS, NBC, and FOX.

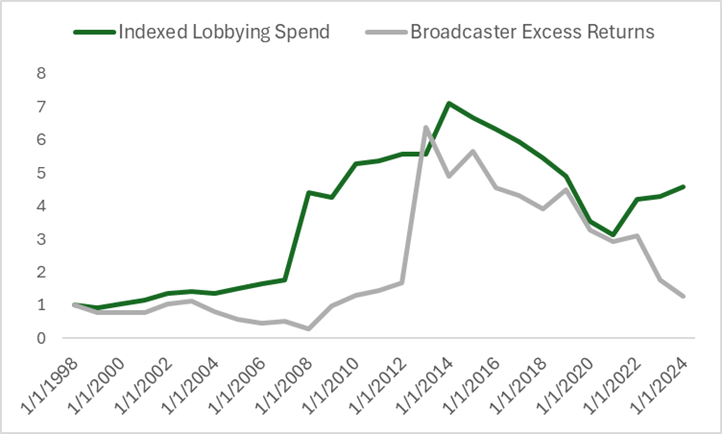

The importance of regulation in the industry likely explains why the National Association of Broadcasters has spent a total of $293M on lobbying since 1998. Of course, the natural question for investors is whether spending money on lobbying is a productive use of capital. Hutchens, Rego, and Sheneman (2016) conduct a broad study that finds a significant positive association between abnormal stock returns and lobbying spend; investors can find the ever-elusive ‘free lunch’ so long as it has been ordered on capitol hill. In figure 2, I plot the evolution in broadcaster lobbying spending against index of average excess returns to a composite of public broadcasters since 1998. Anecdotally, the data would seem to confirm the work of Hutchens, Rego, and Sheneman (2016); benchmark-beating returns appear to co-move with evolutions in lobbying expenditure.

Figure 2: National Association of Broadcaster Lobbying Spend vs. Broadcaster Excess Returns over the S&P 500, Annually 1998 - 2024

Source: Opensecrets.org, S&P Capital IQ, Countervail Analysis

Note: Broadcaster Excess Returns are the equal-weighted average of Sinclair (NasdaqGS:SBGI), Tegna (NYSE:TGNA), Nexstar (NasdaqGS:NXST), and Gray Media (NYSE:GTN) less the S&P 500

Lobbying spending by the National Association of Broadcasters inflected upwards in 2022 after sequential year-on-year declines that began in 2014. There are now signs that the regulatory environment is changing. As of March 11, 2025, the FCC granted Gray Media (NYSE:GTN) a waiver allowing the company to acquire Fox affiliate KLXT-TV in Rochester Minnesota, where Gray Media already operates an NBC station. According to the press release: “This marks the first approval by the FCC for a combination of two top-ranked television stations in the same market in over five years and represents a quick turnaround, as the approval came just two months after Gray requested it.” It’s probably just a coincidence that, for the first time in its corporate existence, Gray Media spent $170K on lobbying efforts in 2023 and $200K in 2024. The legal context for this decision is a 2021 U.S. Supreme Court decision that unanimously upheld the FCC’s authority to modify media ownership rules. This allows the FCC to review proposals granting broadcasters duopoly status in certain markets on a case-by-case basis.

These developments could sponsor a wave of industry consolidation, which would drive considerable cost synergies for broadcasters. These tailwinds arrive as Gray Media and peers trade near all-time lows. Figure 3 shows Gray Media’s TEV/EBITDA and P/BV over time. Today, Gray Media trades at 5.7x EBITDA and 0.2x book value, levels rarely seen outside of the financial crisis. Gray Media carries a substantial amount of debt, so there is some bankruptcy risk, but the company is basically priced for a 2008-like environment at a time when changes in regulatory environment could meaningfully flow through to fundamentals.

Figure 3: Gray Media Valuation Multiples, 2000 – Present

Source: S&P Capital IQ

In sum, Stigler’s rational choice theory of political economy argues that regulations are largely a byproduct of competitive tactics. Empirical studies conducted by finance academics find that lobbying spend can translate directly into attractive risk-adjusted returns. I present the broadcasting industry as one example of an industry where outcomes and excess returns appear to bear a strong positive relationship. While there are many variables at play – most notably the risk of over-levered balance sheets in an uncertain economic environment – it seems the market has yet to price the flow of broadcasting lobbying spend and its potential impact on the industry’s fundamentals.

If you enjoyed this piece, please consider subscribing or sharing.