Broken Compounders

Quality Investors are Long Disruption Risk -- Or, Why TCI's Chris Hohn Sold MSFT

The past 10 years marked a rare Rorschach moment where growth, value, quant, and passive investors aligned on the same strategy: owning high ROE, wide moat businesses with the potential to compound shareholder value over an appreciable time horizon. Buying shares in these ‘good businesses’ became the focal point of a broad and otherwise disparate range of investors that included Berkshire Hathaway, AKO, Baillie Gifford, AQR, DFA, and leading private equity investors. The strategy’s returns are grounded in the idea that competitive advantages persist, and further that earnings power is relatively inelastic to the business cycle. The quality investor’s bet on predictability, however, requires just that: a world in stasis. Here, I reframe the quality premium as compensation for risky secular bets that are exposed to the tail risk of disruptive innovation.

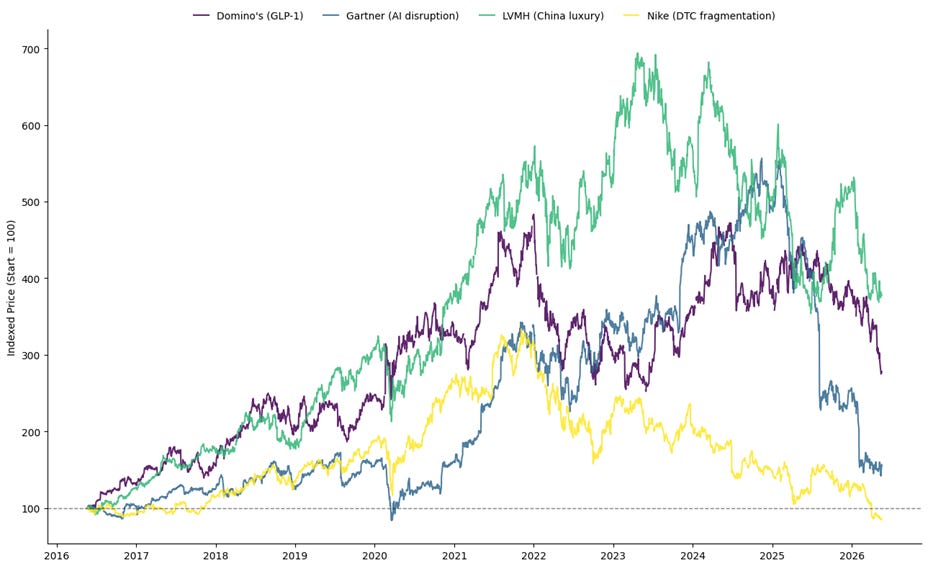

Over the past two years, the quality investing paradigm has been put to the test, with many high-quality firms experiencing considerable drawdowns. Figure 1 shows the share price performance of Domino’s, Gartner, LVMH, and Nike, four high quality businesses with distinct moats that have experienced substantial drawdowns. From 2016 to 2022, shareholders of these firms were up between ~3.0x and ~5.0x. Since 2022, however, each business has faced some form of secular disruption: GLP-1’s, AI, China consumer, DTC unbundling. Domino shareholders are now in a -42.5% drawdown; LVMH shareholders in a -45.5% drawdown; Gartner shareholders in a -71.8% drawdown; and Nike shareholders in a -74.2% drawdown.

Figure 1: Broken Compounders, 2016 – Present

Source: YFinance, Countervail Analysis

Quality-investing is based on the idea that business characteristics are more correlated through time than expected: fantastic businesses slowly become great, and then eventually average. Investors misprice this right tail of business durability, meaning these typically expensive firms are actually cheap relative to their persistent ability to harvest economic rents. Importantly, because the conventional academic explanation implies that quality returns are driven by behavioral mispricing and not incremental risk-taking, shares in wide moat business supposedly offer something of a free lunch. The recent and precipitous share price declines of today’s quality stalwarts, however, suggests that the business quality fade may not be so gentle and the lunch might come with a bit of indigestion.

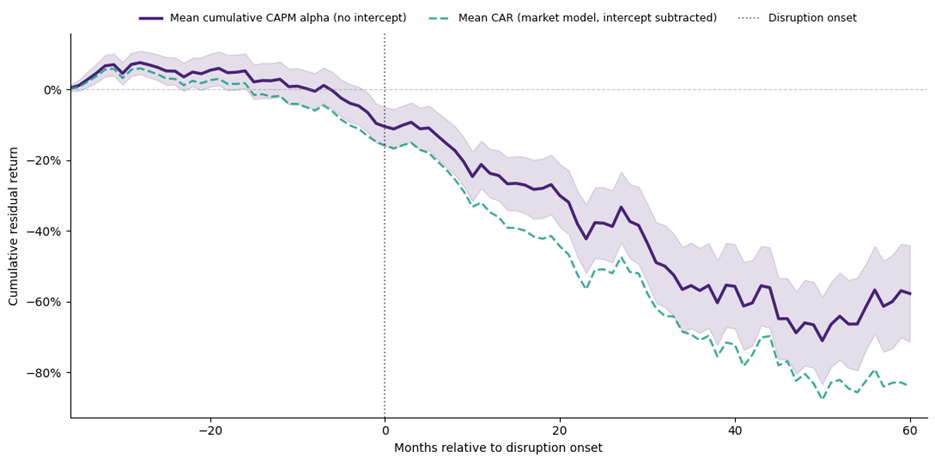

In my view, quality investing is in fact risky. Instead of exposing investors to business cycle risk, however, these firms expose their shareholders to the risk of secular disruption. In other words, behavioral alpha might just be compensation for innovation beta. To study this, I assembled a dataset of ~150 disruption episodes spanning 2000 to 2020 that include a variety of displacements: shale gas displacing thermal coal, SaaS displacing packaged software, smartphones displacing GPS hardware, passive indexing displacing active management. The data highlight a common return pattern: a period of modest economic rent followed by a massive and discontinuous phase of disruption. Figure 2 shows the average cumulative alpha — the residual return left after stripping out each firm’s estimated market exposure — to these businesses pre-and post-disruption. After the onset of disruption, alpha collapses, approaching -75.0% cumulatively after 60 months.

Figure 2: Mean Cumulative CAPM Alpha, Pre and Post Disruption

Source: CRSP/Compustat, Countervail

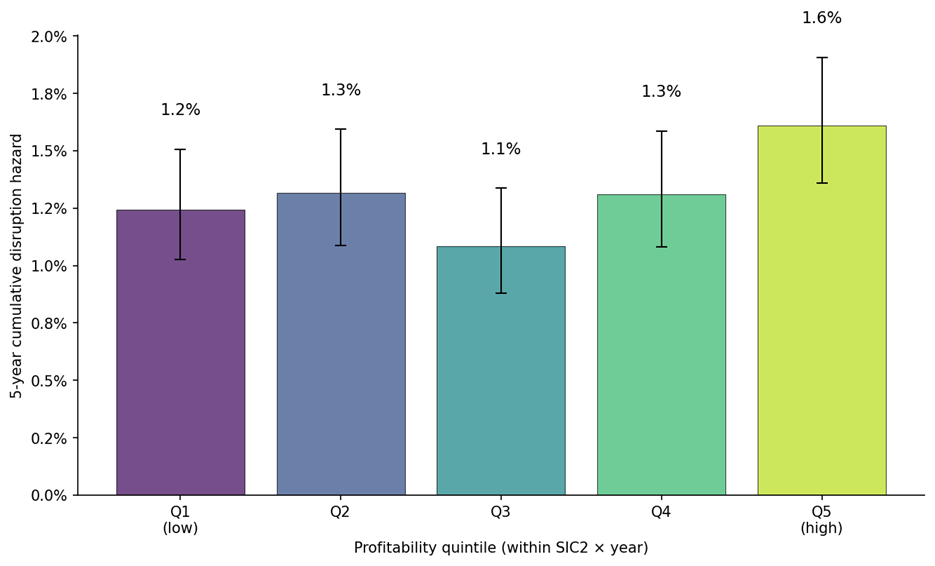

While visually impactful, this study suffers from an obvious bias: I’ve cherry-picked the firms with moats that became observably defunct with the passage of time. But my view that quality investing is risky rests on the simple idea that high rents naturally invite competition, so even within this biased sample, we can measure how disruption frequency changes with business quality. The data in Figure 3 uses the study sample to measure disruption incidence by quality quintiles, which comprise a significantly broader sample of firms. The incidence of disruption is ~30% greater among the highest quality firms, and this difference is significant at the 5.0% threshold.

Figure 3: Disruption Hazard is Increasing in Quality

Source: CRSP/ Compustat, Countervail Analysis

Compared to the full sample of firms, the absolute incidence of disruption is rare, and in aggregate, this explains a small portion of the quality premium. But prior data highlights that the consequences of these events can be catastrophic: -75.0% cumulative negative alpha over 60 months. This would be most pronounced for investors managing concentrated portfolios, or if multiple disruption events arrive simultaneously, as they have in the past few years.

In sum, compounders are implicitly underwritten with a gradualist world view characterized by weak and predictable mean-reversion. In reality, high quality businesses exist in an unstable equilibrium. Competitive moats do not exist along some gradient of advantage, instead they are founded in structural difference that can evaporate with the arrival of a new competitive architecture. This likely explains why TCI’s Chris Hohn recently sold his firm’s position in Microsoft even though the recent financials show accelerating revenue growth and expanding profitability. Hohn believes the business model is broken: “we reduced our investment in Microsoft because the rapid progress in AI introduces uncertainty over Microsoft’s competitive position in the future.” As a concentrated quality investor, Hohn understands that risk management is predicated on managing exposure to secular threats before they begin to materialize in the financials. Otherwise, quality investing can resemble a risky form of carry — a steady premium earned by selling puts on disruptive innovation.